February 6, 2025 | by The Team at Wellby

Fixed or Adjustable-Rate Mortgages: Which Home Loan Is Right for You?

February 25, 2022

By The Team at Wellby

The home-buying process can be pretty overwhelming between finding an ideal home, getting it inspected and appraised, and securing a mortgage. However, there are two primary types of home loan options out there, so you can find the right fit for your financial journey.

To help you determine whether a fixed-rate home loan or adjustable-rate home loan is right for you, we're reviewing the pros and cons of fixed-rate and adjustable-rate mortgages.

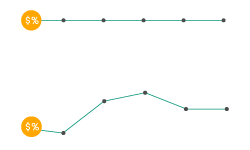

Fixed-Rate Mortgages

What is a Fixed-Rate Mortgage?

A fixed-rate mortgage is a loan that allows you to purchase or refinance a home. As the name suggests, the interest rate on this loan is fixed over the course of the life of the loan. Most commonly, fixed-rate mortgages have terms of 30 years. However, it is not uncommon for people who wish to pay off their loans sooner to take out 10-year or 15-year fixed-rate mortgages.

A fixed-rate mortgage is a loan that allows you to purchase or refinance a home. As the name suggests, the interest rate on this loan is fixed over the course of the life of the loan. Most commonly, fixed-rate mortgages have terms of 30 years. However, it is not uncommon for people who wish to pay off their loans sooner to take out 10-year or 15-year fixed-rate mortgages.

How it Works

While your mortgage payment won't change over the course of the life of the loan, you will pay more toward interest than principal for the first several years. Depending on your interest rate, you may not switch to paying more toward principal than interest until at least seven years into your loan.

When is it the Right Fit?

This type of mortgage is right for people buying their forever home or those planning on staying in their home for at least seven years.

Advantages of Fixed-Rate Mortgages

The most compelling advantage of a fixed-rate mortgage is the low risk associated with taking out these types of home loans. Your monthly payment will not change over the life of the loan, giving you the ability to budget appropriately for your monthly payment.

The most compelling advantage of a fixed-rate mortgage is the low risk associated with taking out these types of home loans. Your monthly payment will not change over the life of the loan, giving you the ability to budget appropriately for your monthly payment.

It may be the perfect choice for people on a fairly tight budget or those who don't feel confident that their income will increase significantly over time. In these circumstances, if you opt for an Adjustable-Rate Mortgage (ARM) and the interest rates increase, it might be very difficult to afford the increased cost of your mortgage, property taxes, and homeowner's insurance.

Disadvantages of Fixed-Rate Mortgages

The most significant disadvantage of a fixed-rate mortgage is that it can cost you a substantial amount. You may pay more interest over the life of your loan than you would with an Adjustable-Rate Mortgage (ARM). This is especially true if you take out a mortgage when interest rates are high and they decrease later.

If you want to take advantage of the low-interest rates, later on, you'll need to refinance your home loan. This isn't much of a problem if there are no prepayment penalties. However, you should consider some of the costs you may have to pay when refinancing, including application and loan origination fees, appraisal fees, recording fees, prepaid property taxes, and more.

Adjustable-Rate Mortgages

What is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage, commonly referred to as an ARM, starts with a fixed rate for a set period of time, typically 3, 5, or 7 years. Once the initial fixed-rate period is over, the rate can shift up or down depending on market conditions.

An adjustable-rate mortgage, commonly referred to as an ARM, starts with a fixed rate for a set period of time, typically 3, 5, or 7 years. Once the initial fixed-rate period is over, the rate can shift up or down depending on market conditions.

The good news is that there are interest rate caps on ARMs which set a limit on how high or how low your rate can go. Typically, there will be a cap on your first and future rate changes, plus a lifetime cap. Adjustable-rate mortgages are most commonly offered with a 30-year term.

How it Works

As you shop around for mortgages, you'll see that ARMs have unique term lengths and limits. For instance, common ARM terms are 3/1, 5/1, 10/1, or 7/1. Each number specifies the fixed vs. flexible rate term. The first number defines the introductory fixed-rate period of the ARM, which can be in months or years. The second number expresses how often your interest rate can be adjusted or changed after the introductory period ends.

When you're looking into various ARMs, you'll see they look something like this:

- 3/1 ARM - The interest rate is locked for three years. After that period ends, the rate may fluctuate every year for the rest of your loan.

- 5/1 ARM - The interest rate is locked for five years. After this introductory period, the rate may be adjusted every year for the remainder of your loan.

- 7/6m ARM - The interest rate remains the same for the first seven years of the loan term. After the first seven years are up, the interest rate is adjusted every six months.

When is it the Right Fit?

This type of mortgage is ideal for people who plan to sell their homes before the fixed-rate term is over. It is also a good option for people with a high-risk tolerance, flexible budget, and a desire to stay in their home for longer than the fixed-rate term.

Advantages of ARMs

An enticing advantage of an adjustable-rate mortgage is a lower initial interest rate compared to a fixed-rate mortgage. Because interest drastically affects your monthly payments, keeping this cost down can have a big impact when budgeting for your new home.

If you have more debt or are looking to take out a larger mortgage loan, the lower payment will help your debt-to-income (DTI) ratio and in turn help you qualify more easily for an ARM than a fixed-rate option. DTI is your monthly payments relative to monthly income, which is calculated by totaling your minimum monthly payments - including the mortgage payment - and dividing by your gross income. DTI is expressed as a percentage.

If you have more debt or are looking to take out a larger mortgage loan, the lower payment will help your debt-to-income (DTI) ratio and in turn help you qualify more easily for an ARM than a fixed-rate option. DTI is your monthly payments relative to monthly income, which is calculated by totaling your minimum monthly payments - including the mortgage payment - and dividing by your gross income. DTI is expressed as a percentage.

Some borrowers will use the lower starting payment of their ARM as a means to buy more house since the payment will be manageable due to the lower rate, which can balance out the higher principal balance. This provides the opportunity to purchase a slightly more expensive or modern home while still keeping your monthly payments within budget.

Disadvantages of ARMs

While the typically lower advertised rate of an ARM is often more attractive than the higher rate of a fixed-rate mortgage, ARMs are riskier because of their adjustable interest rates. Once the fixed-rate period is over, if your interest rate increases, so does your payment.

Many homeowners hedge this risk by making extra payments toward the principal each month during the lower-rate introductory period. With a lower principal balance at the time of a rate increase, the additional interest won't be as high on your future monthly payments since you paid down the principal.

Finding the Right Home Loan for You

While there are differences between a fixed-rate mortgage and an adjustable-rate mortgage, neither is superior. Each has advantages in different circumstances and understanding the differences between the two types of home loans puts the power in your hands. We want to empower you to make the best decision for your unique financial situation and our lending specialists are ready to answer any questions you may have.

While there are differences between a fixed-rate mortgage and an adjustable-rate mortgage, neither is superior. Each has advantages in different circumstances and understanding the differences between the two types of home loans puts the power in your hands. We want to empower you to make the best decision for your unique financial situation and our lending specialists are ready to answer any questions you may have.

Take a look at our mortgage calculator and increase your confidence with the mortgage process by estimating how much your monthly mortgage payment would be based on the type of loan you're interested in, the term length, and interest rates available.

Related Topics

About the Author![Social Icon]()

![Social Icon]()

![Social Icon]()

The Team at Wellby is a diverse group that is here to help you find the right financial solutions for your unique goals and budget. Our passion is people: our members, team members, and the communities we serve. We help people find solutions that support their financial well-being, allowing them to dream and prosper.